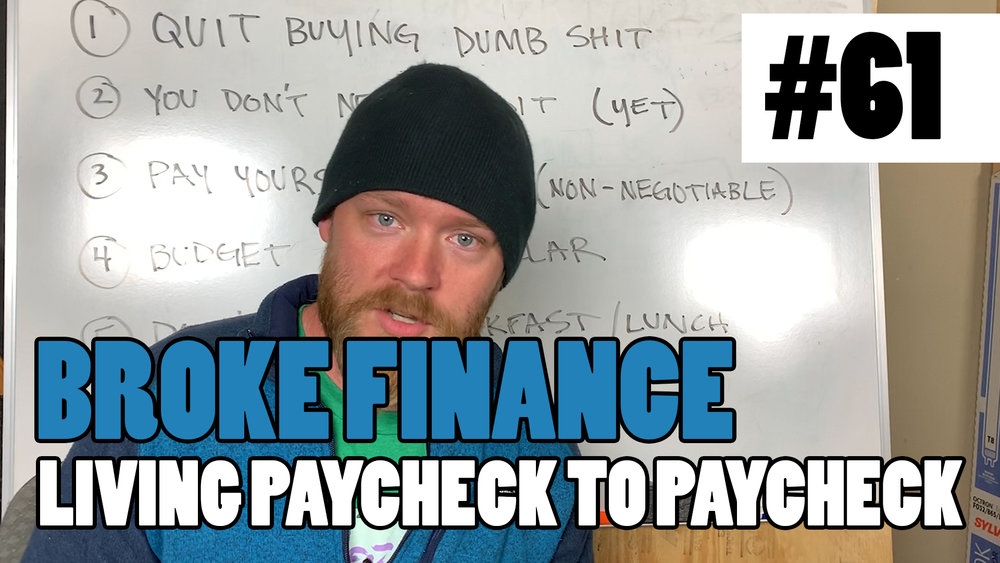

Episode 61 - Broke Finance - 6 STEPS ON HOW TO STOP LIVING PAYCHECK TO PAYCHECK

Episode 61 - Broke Finance - 6 STEPS ON HOW TO STOP LIVING PAYCHECK TO PAYCHECK

Episode 61 - Broke Finance - 6 STEPS ON HOW TO STOP LIVING PAYCHECK TO PAYCHECK

In this episode we talk finances for people who need it the most. If you’ve been living paycheck to paycheck and can never seem to get ahead, this episode is for you. I talk about my 6 foundational tips for how to think about personal finance when you don’t make very much money.

I started this trade as a broke apprentice and a single dad. I had child support to pay, vehicles that were far beyond my means to keep making payments on, and piles of debt and bad decisions that seemed to appear as brick walls to my future. It seemed like every time I turned around I was faced with financial problems, to which I only made worse decisions. I was being reactive to my finances rather than proactive.

To everyone’s credit, we’re not taught this stuff in school. Nobody sits down with us and tells us how to balance a checkbook (yes…those are still a thing"), properly leverage debt, how to get low-interest credit cards, or how to save up for your future.

There are some basic understandings that those with wealth have, that those without lack. Chief among them is that people with money HOLD ON TO THEIR MONEY. That’s how they HAVE money. Most people do not just get a ton of money one day, instead they slowly put aside a little bit here and there until they have a sizable pile. And then they don’t spend it, they invest it so it continues to grow.

My 6 Steps To Stop Living Paycheck To Paycheck

Quit buying dumb shit

You don’t need credit (yet)

Pay yourself first (non-negotiable)

Budget EVERY dollar

Don’t buy breakfast, lunch, or dinner

Build an emergency fund.

#1 - Quit buying dumb shit

What this really means, is you need to start developing more impulse-control. Most of the population of this country fall victim to compulsive spending. This means when we’re at a store to buy water we’re tricked into buying a snickers, 2 energy drinks, a breakfast taco, and a lighter. We spend far more money everyday than we need to because most of us lack the discipline to buy ONLY what we need to. That and we’re advertised to and “suggestively sold” on convenience items as we walk down the aisle of every store we go to. This is the “dumb shit.” You don’t need to buy a $9.99 game add-on for Clash Royale if you’re having trouble keeping your phone line connected. Have some discipline and learn to police yourself on what you give up dollars to. If it’s not absolutely necessary, don’t spend it. Save it instead, you’ll be glad you do when you see that pile start adding up after a few months.

#2 - You don’t need credit (yet)

Credit is an extremely touchy topic, because most of us have far too much of it, or can’t get any of it. For someone who’s having difficulties paying their bills, credit is the worst thing you could get yourself into. You can’t pay your own bills, let alone pay back somebody that you’re borrowing money from. What you need to do is save up little amounts of money over a long time so you can get yourself out from under the strife of being broke all of the time.

We all know a person or two that has flawless credit and they could have anything they wanted because the options they have available to them. The difference is that these people are educated about spending and keeping money and have earned that credit score by borrowing tens to hundreds of thousands of dollars over a decade or more. They EARNED that credit-worthiness by being smart and making smart decisions with money.

#3 - Pay yourself first

This is a big one. You work your ass off everyday to make ends meet, so you should be the one making decisions on where that money disappears to. This doesn’t mean to be delinquent on your debts, but it does mean that you need to make yourself a priority above them. Pay yourself first, before paying any bills. And do this for EVERY paycheck that you cash, for the rest of your life. It doesn’t have to be a lot of money, even a simple $20/wk or $50/two weeks can make a huge difference in a short amount of time. If you always put your bills first, then you are only working FOR your bills. You’re never going to get a grip of money under you to become stable financially, if you don’t pay yourself first. If you’re not doing this, then why on earth are you working in the first place? I don’t know about you but I didn’t choose to be employed so that I could just give it away to other people the rest of my life. I’d rather live a smaller life and have more, than live a big life and have nothing to show for it.

#4 - Budget every dollar

Give every dollar a name. I personally built an excel spreadsheet that allows me to see DAILY where my money needs to go, and it allows me to forecast out every day for the next year. Really, I do 2 years out because I like to see where I’m going to be further than 12 months from now, but it’s a great place to start. If you need help making a budget like this, let me know and I’ll try to help you put one together. If you know where every dollar is going then you won’t frivolously spend outside of your plan. Stick to the plan, it works every time….but only if you stick to it.

#5 - Don’t buy breakfast, lunch, and dinner

Get in the habit of going grocery shopping every 2 or 3 weeks. Even once a month is fine but you may notice your food starting to turn, in which case you’re again wasting money. If you can spend $200/mo on groceries and ONLY eat that, you’ll be saving yourself roughly $400-500 in wasted spending at gas stations, fast-food joints, and restaurants. When you don’t plan meals and buy groceries, you end up surprise-spending roughly $20-30/day - unless you also buy dinner which brings you to around $50/day spent on food. That’s absolutely insane. Don’t be fancy, get the essentials. Get things that you can make a LOT of meals out of and if it helps, spend Sunday cooking for an hour and prep your meals for an entire week. It helps when you’re tired in the morning and just want to grab something and get out the door.

#6 - Build an emergency fund

This is another really important thing to spend considerable effort doing. Get out of the habit of being reactive to shit happening around you in life, and not being able to handle when things come up. If a tire blows, you crack a phone-screen, the AC goes out in your car in the middle of a Texas summer, you want to be able to handle it. If you don’t have an emergency fund you’ll never have a way to get out in front of problems when they happen. Best-case scenario is that you never have to use this fund. This is a fund that you’ll want to keep growing as you age because the more assets you accumulate, the more money you’ll need to have put aside as “insurance.” At first though, $1,000 is a great target to shoot for. Once you hit that, forget the account exists and start a new savings account for other stuff. Pretend you don’t even have that $1,000 and you’ll be sure to keep it for a long time. Congratulations, you’re now a thousandaire! (I know, millionaire sounds better, but my dude…baby steps)

If you enjoy these episodes please click SUBSCRIBE and LIKE these videos! Also check out the podcast on iTunes, Google Play Music, iHeartRadio, OverCast and Stitcher! (<<<---click the links to teleport directly there!)

LISTEN TO AUDIO:

Join Podchaser to...

- Rate podcasts and episodes

- Follow podcasts and creators

- Create podcast and episode lists

- & much more

Episode Tags

Claim and edit this page to your liking.

Unlock more with Podchaser Pro

- Audience Insights

- Contact Information

- Demographics

- Charts

- Sponsor History

- and More!

- Account

- Register

- Log In

- Find Friends

- Resources

- Help Center

- Blog

- API

Podchaser is the ultimate destination for podcast data, search, and discovery. Learn More

- © 2024 Podchaser, Inc.

- Privacy Policy

- Terms of Service

- Contact Us