Age Pension: Do you fit the bill?

Age Pension: Do you fit the bill?

Age Pension: Do you fit the bill?

Age Pension – Demystified

Australians have a long history when it comes to age pension schemes. The first national pension scheme in Australia was formed in 1909 and provided the grand sum of £1 per fortnight for men over the age of 65. As life expectancy for males at the time was around 55 years, most men did not reach the qualifying age and so the pension at the time was very affordable, which is just as well as its funding came out of general revenue.Of course over the intervening years a lot has changed, including making the Age Pension available for women (although initially it was only provided to widows), introducing means testing, and tying the pension payment rates to inflation.

But given that a lot of recent budgetary changes have been focused on the welfare sector, and may or may not have been put in place, retirees and pre-retirees can be excused for feeling some confusion over just what exactly is the make up of the Age Pension in 2014, what are the conditions to receive it, and the eligibility factors involved.

The main features of the Age Pension as it now stands are:

- a basic maximum rate of $776.70 a fortnight for singles and $1,171.00 a fortnight for couples (from September 20, 2014)

- eligibility age of 65 years

- the application of an income test and an assets test, which can reduce the payment rate for those that exceed certain thresholds for each.

Do you Qualify for the Age Pension?

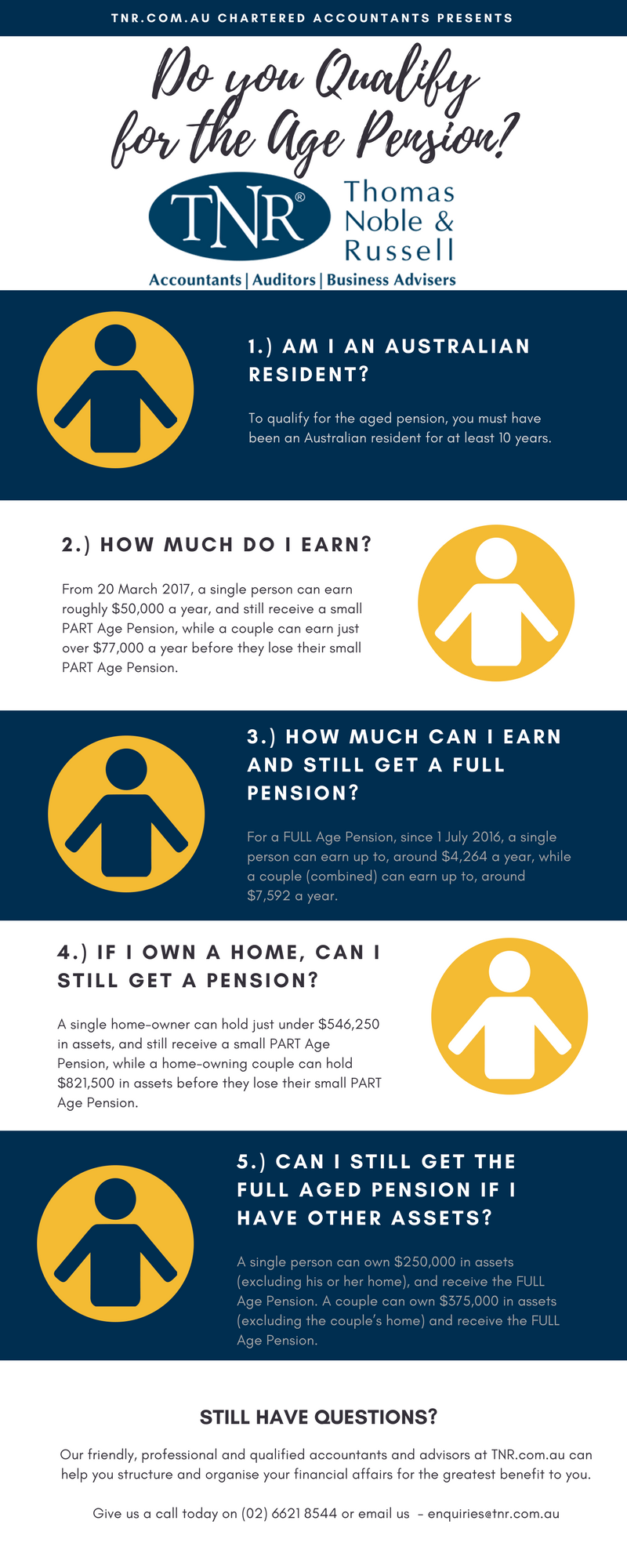

To qualify for the Age Pension, you must first have been an Australian resident for at least 10 years, but you must also satisfy the age, income and assets tests. The Q&A list that follows will hopefully spell out the current status quo, whether you’re eligible, the hurdles to get there, and what benefits you receive.

Q1: What age do I have to be to qualify for Age Pension, and will this change?

A: The current qualifying age for all people, whether male or female, is 65. From July 1, 2017, the qualifying age will increase by six months, and will rise in six month increments every two years to reach age 67 by July 1, 2023. The Federal Government has said that it plans to further increase the eligibility age to 70 by 2035, but this is yet to be legislated.

Q2: What are the means tests to determine how much Age Pension I get paid?

A: The Age Pension payment amounts can be restricted because of income and assets tests. Generally whichever test results in a lower payment is the one that applies to you. If the level of assets or income exceeds the relevant threshold for full benefits, the benefit entitlement is “clawed back”, resulting in a partial pension payment. Of course going over the upper thresholds results in ineligibility for any pension amount. As a reminder about the difference between assets and income, remember that:

- money in the bank is an asset, but the interest it earns is income

- a holiday house is an asset, while the rent it generates is income

- a business or equipment is an asset, while the net profit these make is income.

Age Pension Asset Test

An asset is defined to be “any property or possession you own either partly or wholly”. It includes assets held outside Australia and debts owing to you. Once a person reaches Age Pension age, their superannuation is counted as an asset under the assets test.

Assessable assets typically include:

- amounts in superannuation for persons who have reached Age Pension age

- reportable superannuation contributions (typically salary sacrifice)

- cash and the market value of financial assets held (including interest bearing deposits, fixed deposits, bonds, debentures, shares, property trust units, friendly society bonds and managed investments)

- real estate (including a holiday home) other than the principal home

- total net losses from rental property

- value of businesses or farms including goodwill (where goodwill is shown on the balance sheet), and

- surrender value of life insurance policies etc.

Other assessable assets are more obvious, and include items such as boats, caravans, motor vehicles and other household contents and personal effects.

The asset test limits are also determined by a person’s home ownership status. For home owning singles, the value of all eligible assets must be less than $202,000 for a full pension, or $771,750 for a part pension. For non-home owning singles, the value limits are $348,500 full pension and $918,250 part pension.

For couples, the full pension asset value limit is $286,500 for home owners ($1,145,500 part pension) and $433,000 for non-home owning couples ($1,292,000 part pension).

There are however some excluded assets, which include but are not limited to:

- the applicant’s principal home, or proceeds from the sale of it if it is intended to buy another within 12 months

- assets used to support some income streams, depending on date of purchase

- accommodation bonds paid for residential aged care

- life interest (not created by the pensioner, beneficiary or their partner), and

- granny flat interest.

There are other excluded assets, which Centrelink will be able to determine depending on personal circumstances.

Age Pension Income test

The income test allows for full benefits to be paid where a recipient’s income does not exceed a certain threshold. For singles (from September 20, 2014) this is up to $160 a fortnight, and for couples $284 (for the combined couple). For income above these thresholds, the benefit reduces by 50 cents for each additional dollar of income. Payments reduce to zero at or above the maximum income threshold, which is presently $1,868.60 a fortnight for singles and $2,860.00 for couples.

Q3: I know that to receive Age Pension, I have to be an Australian resident. What exactly constitutes being an Australian resident?

A: To lodge an Age Pension claim, you must be an Australian resident and in Australia on the day that you lodge your claim. To qualify as an Australian resident that can receive Age Pension, you must be living here as:

- an Australian citizen, or

- the holder of a permanent resident visa, or

- a New Zealand citizen who was in Australia on February 26, 2011 or for 12 months in the two years immediately before that date, or was assessed as “protected” before February 26, 2004.

To meet the Age Pension requirements, you also need to fulfil the 10-year qualifying Australian residence requirements, except in special circumstances. This means you have been an Australian resident for a continuous period for at least 10 years, or for a number of periods which total more than 10 years, with one of the periods being at least five years.

Q4: Once I’ve found out that I fulfil all criteria, how do I apply for my Age Pension payment?

A: You should submit your claim to the Department of Human Services (Centrelink) as soon as possible so that you can be paid from the earliest possible date. When lodging your claim you will need to provide details of your income and assets, you partner’s income and assets as well as details of any overseas pension you receive.

You can either claim online by registering for Centrelink’s online services or fill in an Age Pension claim form, which Centrelink can provide.

Once you submit your claim, you will need to provide proof of identity, usually in the form of an Australian birth certificate or authorised extract, a current Australian passport, a citizenship certificate, an Australian visa, a document of identity, a certificate of evidence of resident status or a certificate of identity.

Centrelink will also tell you if there are other verification documents and forms that you need to provide. Centrelink will then send you a letter advising if your claim has been successful or not, which will also outline when your payment will start and how much you will get.

Q5: What are the payment rates?

A: The rates, from September 20, 2014, are as below:

StatusPension rate per fortnightSingle$776.70 (plus clean energy supplement, $14.10)Couple$585.50 each (plus clean energy supplement, $10.60)The next rate adjustment is due in March 2015.

There are additional amounts that may be added to the above, depending on personal circumstances, such as a pension supplement if you are also receiving other support such as a carer payment, bereavement allowance or Austudy. Centrelink can provide more guidance on this, as it will depend on your circumstances.

Q6: Will my payment be adjusted or reviewed?

A: From time to time, your Age Pension payment amount will be reviewed. The amount you receive may be adjusted because your or your partner’s circumstances change. This includes a change in income, accommodation or separation from your partner due to illness.

The Age Pension rate is also adjusted twice a year in line with inflation, usually in March and September. This includes adjustments in line with the Consumer Price Index (CPI), Male Average Weekly Total Earnings, and the Pensioner and Beneficiary Living Cost Index increases. The last is designed to index base pension rates when the cost of living index is higher than the CPI.

Q7: If I am eligible for the Age Pension …

A: You will be paid every fortnight. The Age Pension can include pension supplements to assist with the costs of regular bills such as energy and rates. You will also receive a Pensioner Concession Card to help reduce the costs for medicines under the Pharmaceutical Benefits Scheme. It may also make you eligible for a range of additional concessions. If you are privately renting your accommodation, you may also receive some rent assistance for this cost.

Q8: If I am not eligible for the Age Pension …

If you are deemed ineligible, you always have the right to appeal any decision made by Centrelink. You may still qualify for a Commonwealth Seniors Health Card and this will assist you with the costs of prescription medicines and other health care services. It is not assets tested but an income test applies, which is to be expanded from January 1, 2015, to include superannuation benefits.

The post Age Pension: Do you fit the bill? appeared first on TNR Chartered Accountants Lismore Ballina Accounting, Tax Audit.

Join Podchaser to...

- Rate podcasts and episodes

- Follow podcasts and creators

- Create podcast and episode lists

- & much more

Episode Tags

Claim and edit this page to your liking.

Unlock more with Podchaser Pro

- Audience Insights

- Contact Information

- Demographics

- Charts

- Sponsor History

- and More!

- Account

- Register

- Log In

- Find Friends

- Resources

- Help Center

- Blog

- API

Podchaser is the ultimate destination for podcast data, search, and discovery. Learn More

- © 2024 Podchaser, Inc.

- Privacy Policy

- Terms of Service

- Contact Us